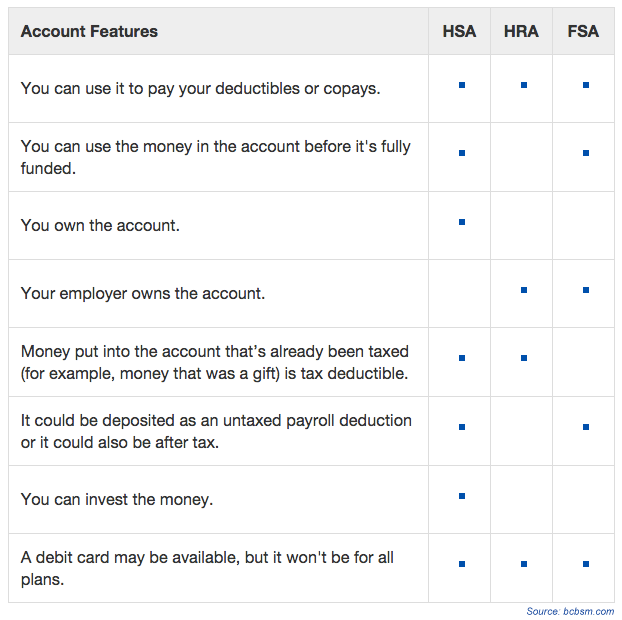

Is An HSA Right For You?

Over the past ten years, Health Insurance has been a hot-topic issue in political arenas and dinner tables alike all throughout the country. From navigating the Affordable Care Act (ACA) regulations and compliance details to researching the available insurance offerings themselves, individuals all over are trying to find the best plan benefits for their budget.

Could an HSA be just the thing?

What Is An HSA?

A Health Savings Account is more commonly referred to as an HSA. An HSA is designed to act as a tax-deferred savings account to help you cover out-of-pocket expenses. It can even be used for non-covered insurance expenses provided they fall under the IRS Qualified Medical Expense (QME) list. This list includes elective procedures, such as Lasik eye surgery.

The general idea is that every month you contribute a set amount into your account and as your HSA grows you receive added financial protection for future healthcare needs, while also tax-sheltering more money. This is a win-win. Many banks will also allow you to invest the money you save into Mutual Funds for higher returns.

In order to take advantage of an HSA, you must first participate in an HSA-compatible plan, better known as a High Deductible Health Plan (HDHP).

Adding Additional Benefits To Your Health Plan

Unlike a traditional savings account HSA’s have a triple tax benefit:

- The contributions that go into your HSA are not taxed.

- Any interest your HSA earns is tax-free

- If you make a withdrawal on your HSA to help cover the cost of a qualified medical expense, you can rest easy knowing that that money will also be tax-free.

Another benefit of an HSA is the fact that there is no deadline on when you need to use the money in your account. Because of this, many are reaping the benefits of their HSA’s well into retirement.

Making The Decision

Ultimately, the only person who can decide if an HSA is right for you, is you. In some cases, your employer might even offer a contribution match to your HSA account up to a certain dollar amount per year, which could help your savings out if you are already putting in the maximum as indicated by the IRS.